(Version in Español)

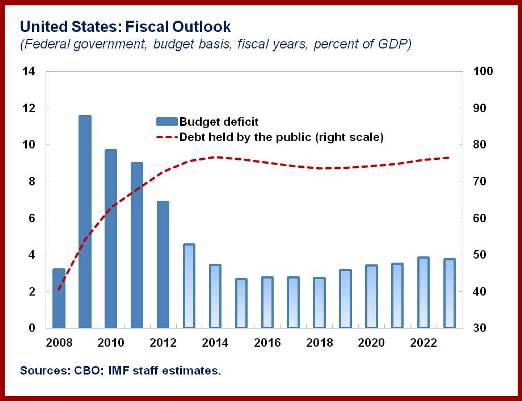

Much has changed on the fiscal front since we started worrying about U.S. fiscal sustainability. The federal government budget deficit has fallen sharply in recent years―from almost 12 percent of GDP in 2009 to less than 7 percent in 2012. And recent budget reports show that the deficit is shrinking faster than expected only a few months ago, to a projected 4½ percent of GDP for the current fiscal year, which ends September 30. Plus, health care cost growth has slowed down dramatically since the Great Recession, alleviating the pressure on public health care programs at least temporarily.

Does this mean we can stop worrying? Not quite. Recent developments certainly mean that things are better than we thought just a few years ago and the fiscal adjustment needed to restore sustainability is smaller. But if the choice and timing of policy measures is not right, the deficit reduction may turn out to be too much in the short run—stunting the economic recovery—and not enough in the long run.

So, in our recent annual check-up of the U.S. economy, our advice is to slow the pace of fiscal adjustment this year—which would help sustain growth and job creation—but to speed up putting in place a medium-term road map to restore long-run fiscal sustainability.

Slow down…

Around this time last year, we were worried that U.S. policymakers would allow a number of temporary tax cuts to fully expire and let significant across-the-board spending cuts (known as the “sequester”) to kick in on January 1, 2013. The combined effect of these measures, dubbed the “fiscal cliff,” could push the economy back into recession.

Congress partly averted the fiscal cliff, with legislation passed just hours before the January 1 deadline: tax cuts were permanently extended for taxpayers below a certain income threshold, but the sequester was only delayed temporarily and allowed to take effect on March 1, 2013.

Budget cuts under the sequester are coming at a time when the economic recovery is still fragile and they are also indiscriminate, affecting many vital services in education, science, and infrastructure. The sequester was intended to be so undesirable that policymakers would be forced to compromise and agree on more sensible options, but that did not happen. IMF estimates suggest that if the sequester did not happen, real GDP growth in 2013 would have been half a percentage point higher.

…Yet hurry up

The silver lining is that the longer-run fiscal outlook today is not as intimidating as it was just a few years ago.

In 2010, the IMF projected an unsustainable trajectory for public debt—the federal government debt ratio could reach levels unseen since the Second World War (close to 100 percent of GDP). Since then, Congress passed several pieces of legislation―one of which led to the events that brought about the sequester. Today, the projections look markedly better (see chart). The federal debt in 2020 is now anticipated to be about 20 percentage points below what it was projected to be back in 2010.

In 2010, the IMF projected an unsustainable trajectory for public debt—the federal government debt ratio could reach levels unseen since the Second World War (close to 100 percent of GDP). Since then, Congress passed several pieces of legislation―one of which led to the events that brought about the sequester. Today, the projections look markedly better (see chart). The federal debt in 2020 is now anticipated to be about 20 percentage points below what it was projected to be back in 2010.

Despite the substantial improvement, the long-term outlook remains challenging. This is because of the impact of population aging, rapid growth in health care costs, and the anticipated increase in interest rates. Spending on Social Security and major health care programs, even considering the recent slowdown, is expected to increase by close to 2 percentage points of GDP over the next decade. A similar increase is projected for net interest outlays, as interest rates gradually normalize.

Hence, with no further actions to raise revenues and reduce entitlement spending, the public debt ratio would start rising again―and this time, from a relatively high starting point.

What should be done?

The key priority for the United States is to implement a deficit reduction plan to curb the pressure that emerges around mid-decade, when the economic recovery is complete, interest rates return to historical norms, and demographic pressures kick in. This plan should:

Easier said than done?

Considerable disagreements exist across the political spectrum on what a deficit reduction plan should look like—hence, the continuing lack of a comprehensive plan. Negotiations so far, however, have shown that there is common ground that can form the basis for a bipartisan blueprint.

So, our message is: explore the options to replace the sequester and fine-tune the pace of fiscal adjustment so that no harm is done to economic growth, and enact laws today that will address the medium-term threats to fiscal sustainability.